Amrit Kaal: The Path to Becoming the 3rd Largest Economy

Amrit Kaal: The Path to Becoming the 3rd Largest Economy

India has been in the spotlight for its ambitions to become a global economic powerhouse with remarkable growth and potential. The country aims to become the world’s third-largest economy. However, this path has its challenges.

Prime Minister Norendra Modi introduced the term ‘Amrit Kaal’ during his address on India’s 75th Independence Day in 2021. He explained that the goal of Amrit Kaal is to propel India and its citizens towards new heights of prosperity and that this period encompasses the next twenty-five years.

India has pursued economic development initiatives and reforms to achieve its goals. The country has made remarkable progress in diverse manufacturing, services, and technology sectors. These efforts have positioned India as a significant player in the global economy.

India has made significant strides in its pursuit to become the world’s third-largest economy. However, despite its considerable progress, several formidable obstacles remain to overcome. It is well-established that all nations encounter hurdles when endeavouring to stimulate economic growth. In this regard, it is imperative to examine the four largest economies in the world, their principal drivers of development, and how India’s economy compares with them before scrutinizing the challenges India currently faces.

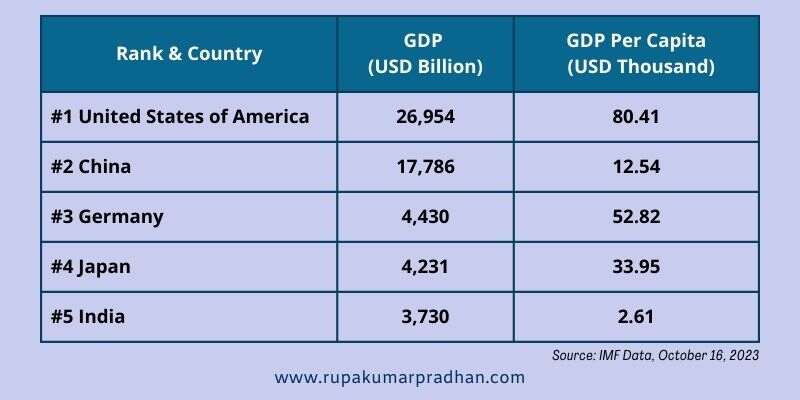

Top 5 Largest Economies in the World 2023

What are the top 5 GDP countries in the world? In 2023, the top five countries will be the United States, China, Japan, Germany, and India. Let’s take a look at the top 5 wealthiest countries in the world in 2023, according to IMF data as of October 16, 2023:

I am pleased to inform you of some excellent news for us. India’s GDP reportedly crossed the $4 trillion mark or Rs. 332 lakh crore for the first time on November 19th 2023.

Let’s analyze the factors that contribute to the growth of all four countries.

#1 USA.

The United States has held the title of the world’s largest national economy in terms of GDP since approximately 1890. The history of the US economy is a captivating story influenced by several significant factors. These drivers have played a pivotal role in shaping the current state of the economy, making it what it is today.

Innovation has been a critical driver of the American economy throughout history. From Thomas Edison’s invention of the light bulb to Steve Jobs’ creation of Apple, American innovators have consistently pushed boundaries and transformed industries, which has helped drive economic growth.

Entrepreneurship has long been a driving force in the US economy, with a culture encouraging individuals to start their own businesses and take risks. This spirit has led to the creation of countless jobs and fueled economic expansion.

Trade has had a substantial impact on the US economy. The country’s abundant resources, advantageous location, and robust infrastructure have made it a desirable centre for global trade. International trade deals like NAFTA (North American Free Trade Agreement) have also increased economic activity by simplifying business with neighbouring countries.

Furthermore, government policies and regulations have profoundly impacted the US economy. Policies promoting free markets, deregulation, and tax incentives for businesses have all contributed to economic growth over time.

Technology has emerged as a significant driver of the US economy in recent years. The rise of digital platforms, e-commerce, and artificial intelligence has revolutionized industries and created new growth opportunities.

Currently, the US economy faces both challenges and opportunities. With ongoing technological advancements and globalization trends, adapting to change is crucial for sustained economic success. Additionally, addressing income inequality and ensuring inclusive growth are important considerations for policymakers.

The United States of America

- GDP: $26,954 billion

- GDP By Country Per Capita: $80,410

- Annual GDP Growth Rate: 1.6%

The United States has maintained its position as the world’s leading economy and the wealthiest country for over six decades, from 1960 to 2023. The US economy is renowned for its exceptional diversity, boosted by significant sectors such as services, manufacturing, finance, and technology. It is home to an important consumer market, encourages innovation and entrepreneurship, has a robust infrastructure, and offers favourable business conditions.

#2 China

China’s economy has undergone remarkable growth and transformation from its agricultural beginnings to becoming one of the world’s largest economies.

China’s economy has rapidly developed due to several key drivers. One of the primary factors is the country’s massive population, which has provided a vast labour force and consumer market. China’s strategic focus on infrastructure development, technological advancements, and industrialization has also significantly propelled its economic growth.

The Republic of China

- GDP: $17,786 billion

- GDP By Country Per Capita: $12,540

- Annual GDP Growth Rate: 5.2%

China has witnessed a notable upsurge in its economic progress, moving from the fourth rank in 1960 to the second rank in 2023. The Chinese economy predominantly hinges upon manufacturing, exports, and investment. It proudly possesses an extensive workforce, robust governmental backing, infrastructural advancements, and an expeditiously expanding consumer market.

#3 Germany

Germany is a global powerhouse with a rich history and a strong economy. Its fascinating past and thriving economic landscape are prime examples of success and resilience. Critical drivers have contributed to Germany’s growth and stability, making it a force to be reckoned with in the global market.

When examining Germany’s economy, one must recognize its historical significance. Following the devastation of World War II, Germany underwent a remarkable transformation into one of the world’s leading economies. Through meticulous planning and hard work, Germany rebuilt itself from the ground up, focusing on industries such as manufacturing and engineering.

Today, German industries are known for their precision and quality craftsmanship. The country is renowned for its automotive sector, led by globally recognized brands like BMW, Volkswagen, and Mercedes-Benz. The engineering industry is also crucial in driving Germany’s economy forward.

Germany’s success is driven by several factors, including a highly skilled workforce and robust infrastructure. The country places significant importance on education and vocational training programs that equip individuals with practical skills necessary for various industries. This focus on skills development has undoubtedly contributed to Germany’s economic prosperity.

Germany:

- GDP: $4,430 billion

- GDP By Country Per Capita: $52,820

- Annual GDP Growth Rate: -0.1%

The German economy strongly focuses on exports and is renowned for its precision in the engineering, automotive, chemical, and pharmaceutical sectors. It derives advantage from its proficient labour force, robust research and development initiatives, and a pronounced commitment to fostering innovation.

#4 Japan

Japan’s economy has a dynamic and rich history, shaped by critical drivers that fueled its growth. From the reconstruction after World War II to technological advancements, Japan has consistently demonstrated resilience and adaptability in its economic development.

Japan’s economy has been driven by its emphasis on innovation and technological advancements. The country has pioneered the automotive manufacturing, electronics, and robotics industries. This focus on innovation has enabled Japan to remain competitive in the global market and cement its position as a technology leader.

Another critical driver of Japan’s economic growth is its export-oriented solid approach. The country is known for its exports of automobiles, electronics, machinery, and other high-quality products. This export-driven strategy has helped Japan build a robust trade surplus and establish itself as one of the world’s largest exporters.

Japan:

- GDP: $4,231 billion

- GDP By Country Per Capita: $33,950

- Annual GDP Growth Rate: 1.3%

Japan is known for its advanced economy, innovative technology, strong manufacturing capabilities, and robust service sector. The country’s most important industries include automotive, electronics, machinery, and finance. Japan is well-known for its strong work ethic, pioneering technological breakthroughs, and top-quality exports.

To truly appreciate Japan’s economy today, it’s essential to understand its history and the critical drivers that have propelled it forward over time. Today’s vibrant economy results from innovation-driven industries, export-oriented strategies, government policies, and ongoing efforts to address current challenges. All these factors have contributed to shaping Japan’s economy into what it is today.

#5 India

India’s economy has been shaped by its rich and complex history, influenced by various factors from ancient civilizations to colonial rule.

India’s population is a critical factor in driving its economic growth. With over 1.4 billion people, India has a massive consumer market and a significant workforce. This demographic advantage has increased foreign investment and domestic consumption, contributing to the expansion of the Indian economy.

India’s diversified economy is a significant factor in its success. The country is recognized for its proficiency in multiple sectors, such as information technology, services, agriculture, pharmaceuticals, and manufacturing. This diversity is vital in mitigating risks from relying too much on a single industry and ensures overall economic stability.

India

- GDP: $3,730 billion

- GDP By Country Per Capita (Nominal): $2,610

- Annual GDP Growth Rate: 5.9%

India is ranked 5th in the world’s GDP rankings in 2023. India’s economy boasts diversity and swift growth, fuelled by critical sectors such as information technology, services, agriculture, and manufacturing. The nation capitalizes on its broad domestic market, a youthful and technologically adept labour force, and an expanding middle class.

The service sector contributes more than 50% to the GDP and is the fastest-growing sector. In contrast, the industrial and agricultural sectors employ most of the labour force.

The government is taking action to become the world’s 3rd largest economy.

- Credit growth for the Micro, Small and Medium Enterprises (MSME) sector has remained consistently high, averaging over 30.5% from Jan to Nov 2022.

- The central government’s capital expenditure (Capex) increased by 63.4% in the first eight months of FY23, which contributed significantly to the growth of the Indian economy in the current year.

- Private consumption accounted for 58.4% of GDP in Q2 FY23, the highest since 2023-24. The increase was supported by a resurgence in contact-intensive services such as trade, hotels, and transportation.

Union Minister Hardeep Singh Puri stated that India aims to increase its manufacturing share in GDP from 17% to 25%.

Hardeep Singh Puri addressed the 118th Annual Convention of the PHD Chamber of Commerce and Industry (PHDCCI). He mentioned that global supply chains are currently realigning, and India is emerging as a favourable alternative source for supplies. This is due to India’s abundant raw materials, low labour costs, growing manufacturing know-how and entrepreneurial ability.

India focuses on every driver of GDP, including consumption, private investments, government spending, and net exports.

India, the land of diversity and opportunity, is poised to become the third-largest economy in the world. While some may question the feasibility of this claim, a closer look at India’s economic growth trajectory reveals a compelling case for its rise.

India’s economy is expected to become the world’s third-largest. With an increasingly ageing population, there is a pressing need for retirement planning. As a result, it is essential to develop sound strategies that consider the unique challenges posed by India’s ever-changing economic landscape. Individuals can ensure their financial security during their golden years and contribute to the nation’s continued prosperity.

India’s economy is expected to become the world’s third-largest. With an increasingly ageing population, there is a pressing need for retirement planning. As a result, it is essential to develop sound strategies that consider the unique challenges posed by India’s ever-changing economic landscape. Individuals can ensure their financial security during their golden years and contribute to the nation’s continued prosperity.

I want to bring to your attention some unsettling retirement statistics. According to a recent survey conducted by Sambodhi Research and pinBox Solutions, over half of Indians (52%) anticipate relying on their children for financial support in their old age. In comparison, 28% have yet to begin saving for retirement.

Did you know that over 65% of India’s population is under the age of 35? Out of the total population of 1.4 billion, 910 million people will retire after 25-30 years. This scary retirement statistic makes us wonder about the future. Are you financially prepared to face the challenges of retirement?

If you’re a millennial, generation-Z or nearing retirement, striving for a secure future, “JOYFUL RETIREMENT: The 7-Step Strategy for Healthy, Wealthy, and Early Retirement” could be the perfect solution. With this book, you can feel empowered to create a retirement plan that gives you confidence and peace of mind.

One of the key factors contributing to India’s potential as a global economic powerhouse is its demographic advantage. With a young and dynamic population, India has a vast workforce that can fuel growth across various sectors. This demographic dividend provides India with a competitive edge over ageing economies.

India has been making significant progress in economic reforms and policies to attract foreign investment. The country has attracted FDI inflows worth $70.97 billion in FY 2022-23, with FDI equity inflows amounting to $46.03 billion. Mauritius (26%), Singapore (23%), USA (9%), the Netherlands (7%), and Japan (6%) are the top five countries for FDI equity inflows into India during this fiscal year. The government’s initiatives, such as Make in India and Digital India, have created a favourable investment climate that encourages domestic and international businesses to establish operations there.

According to a report by CII-EY on FDI, India has the potential to attract FDI between $120-$160 billion annually by 2025.

India has become a hub for innovation and technology-driven industries. The country has a thriving startup ecosystem that has given rise to many unicorns across different sectors, such as e-commerce, fintech, and health tech. These innovative ventures create job opportunities and drive economic growth through their disruptive business models.

Moreover, India is strategically positioned geographically with access to major international markets. Its strong trade relationships with countries worldwide enable it to leverage global opportunities for trade and investment.

While challenges such as infrastructure development and socio-economic disparities still exist, the Indian government has recognized these hurdles. It is actively working towards addressing them through initiatives like Smart Cities Mission and rural development programs.

“India’s economy is a sleeping giant. Once it awakens, it will be a force to be reckoned with” ~Jack Ma, Chinese Business Magnate and Philanthropist.

Considering all these factors, it becomes evident that India has immense potential to become the third-largest economy in the world. However, achieving this milestone will require continued efforts in skills development, infrastructure enhancement, and inclusive growth policies.

In conclusion, while there may be sceptics questioning whether India can become the third-largest economy globally when considering its demographic advantage, pro-business reforms, technological advancements, strategic positioning in international markets coupled with the government’s commitment to addressing challenges, it becomes apparent that India is on a path towards achieving this milestone.

India has made significant strides in the direction of becoming the world’s third-largest economy, as per recent reports. India’s remarkable economic growth can be attributed to the country’s diverse and skilled workforce, its increasing competitiveness in global markets, and its significant contributions to the world’s technological advancements. With continued investments in infrastructure, education, and innovation, India is poised to achieve even greater economic success in the years to come.

Are you making strides towards achieving financial freedom through investment in tandem with India’s economic growth? Assessing whether you are on the right track to meet your financial goals is imperative. India’s economy has been experiencing a steady growth trajectory, making it a promising destination for investors. To ensure you are on the right track, you must evaluate your investment strategy regularly or start investing today.

Embrace the dawn of prosperity with Amrit Kaal!

Keep moving forward and keep investing in your future!

I am a CERTIFIED FINANCIAL PLANNERCM and CHARTERED WEALTH MANAGER®, dedicated to helping my clients achieve financial freedom and experience the joy of being in the HappyMoney Zone. For the moment, I have shared my experience growing up with you because it had a tremendous impact on how I do what I do. If you have a question about your financial situation, please connect me. I would be delighted to try to be of service. Don’t miss any future posts; please subscribe via email.

Hello! Connect with Mr. Rupakumar Pradhan, CFP, CWM, by filling out the form linked below. Form Link:https://forms.gle/dhuYuUp7Uri5cB9U9

Do you need asset allocation? Read it.